Attention: You need JavaScript enabled to use this site.

As a mortgage lender we strive to make sure we offer the best possible value, both during any product period and beyond. That’s why when your mortgage with us comes to the end of its product offer period and you have not yet chosen another product offer to switch your mortgage to, your mortgage will revert to a variable interest rate.

This variable interest rate will be the Society’s Standard Variable Rate (SVR) with a potential reduction applied dependent on your Loan to Value (LTV). This means that as a result of any increase in the value of your home or any reductions you make to your mortgage balance which reduces your LTV, you may benefit from a lower variable interest rate being charged.

ⓘ Standard Variable Rate - The Standard Variable Rate (SVR) is a variable rate of interest set independently by the Society which may be updated from time to time as outlined in the Society’s Mortgage Conditions.

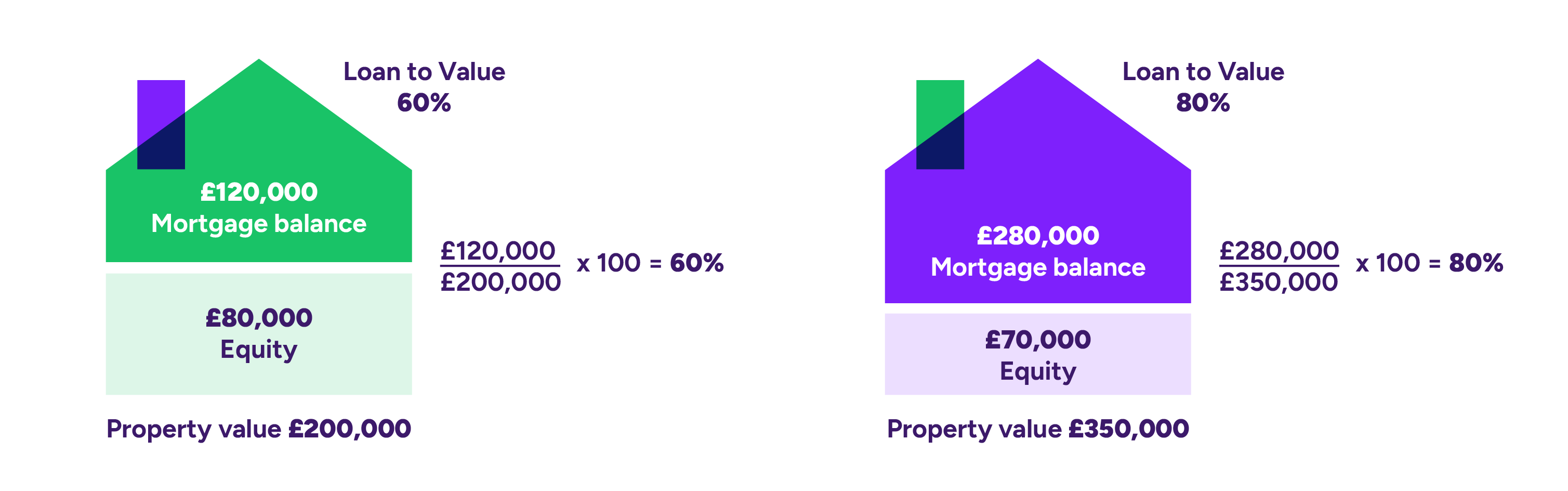

ⓘ Loan to Value - Your Loan to Value (LTV) is the value of your property compared to the size of your outstanding mortgage balance. For example, if a property is valued at £200,000 and the mortgage balance is £120,000, the LTV would be 60% as the outstanding mortgage balance is 60% of the value of the property.

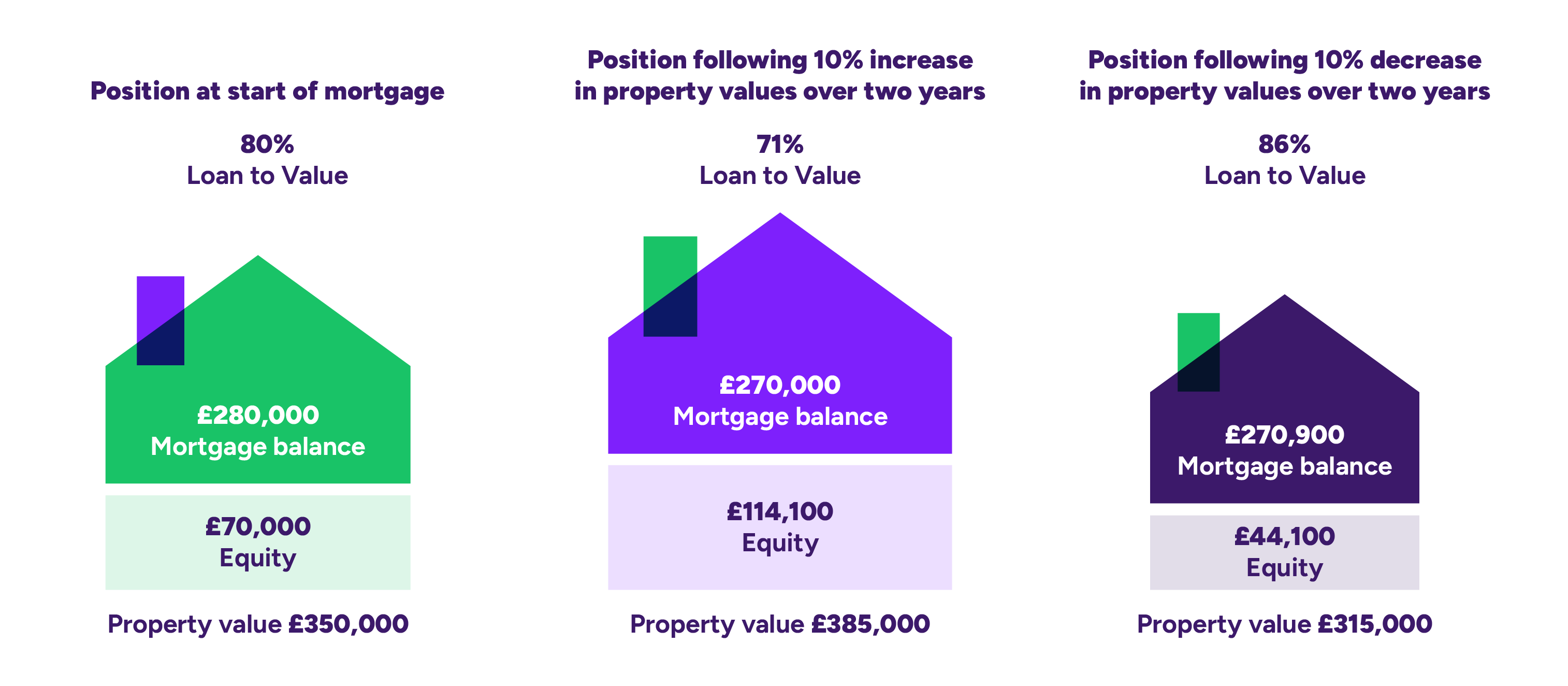

Please be aware that your LTV can increase or decrease if there are any changes to the value of your property or outstanding mortgage balance.

The Loan to Value is calculated in the following way:

Examples of different Loan to Value calculations are shown below.

These examples are for illustrative purposes only.

ⓘ Property equity is the difference between what you owe on your mortgage and the current value of your property.

Before the end of your mortgage product term we will write to you so you can consider whether you want to switch to a new mortgage product deal. If you choose not to switch to a new mortgage product deal, you will be automatically transferred to a variable interest rate, which will be determined by your Loan to Value (LTV) at that time. You might find it helpful to refer to your mortgage Illustration which sets out the length of your product offer period.

If your LTV is greater than 85% you would revert to the Society’s Standard Variable Rate (SVR), currently 6.24% variable. As your LTV reduces you may benefit from the lower variable interest rates outlined in the table below.

The rate when your product offer period ends uses the LTV of your property to calculate the rate of interest you would pay.

| Loan to Value % | Variable interest rate payable |

|---|---|

| Greater than 85% | 6.24% (Society’s SVR) |

| Greater than 75% but less than or equal to 85% | 5.74% |

| Less than or equal to 75% | 5.49% |

Below are examples of how the LTV can change over a two year period when the value of a property goes up or down.

These examples are for illustrative purposes only.

We have outlined below some of the changes that would affect the Loan to Value and when this would affect your mortgage payment.

| Changes that would affect your mortgage at the time a change occurs | Changes that would affect your mortgage on an annual basis |

|---|---|

The Society will assess what the Loan to Value (LTV) and variable interest rate would be straight away when the following changes happen to your mortgage. These are:

|

The Loan to Value (LTV) and variable interest rate will be reviewed in March every year which means that there may be changes from the previous 12 months that could affect the rate you are on. These are:

|

* We regularly review the UK House Price Index (UK HPI) which measures changes in the value of residential properties. We will use the latest valuation information we have to assess what your approximate LTV is when we undertake our annual review of your variable interest rate. If there have been any improvements made on your home, these may not be reflected in the LTV we use. If this is the case or you believe the valuation is inaccurate, then we can revalue your property, however there will be a fee for carrying this out. To find out more call us on 0345 241 1723.

The Loan to Value (LTV) for your whole mortgage balance, which includes the additional borrowing, will be used to calculate the applicable variable interest rate for any part of your mortgage that is outside of a product offer period. This will be the Society’s Standard Variable Rate with a potential reduction applied dependent on your LTV.

We will write to you to let you know what your new monthly mortgage payment will be.

The Society will undertake an annual review and re-calculate what the variable interest rate is in March every year. We will notify mortgage customers who are on the variable interest rate if their mortgage payment has changed as a result of their Loan to Value (LTV) changing since the last review. You will only be contacted if there are any changes to your mortgage payment.

We will also provide you with notice should we discontinue the use of your LTV when calculating your mortgage payment.

You can call us on 0345 241 1723 (lines are open Monday to Friday 8.30am to 6.00pm) or send us a message and one of our experts will get back to you.